In this video I explain how much financial aid I received from nys student loans. Let me know what you think! Love you guys! Make sure to subscribe if you haven’t already. Thank you for watching! nysstudents nysschoolloans

This week we talk about education financing in New York State. We also discuss the pros & cons of tuition tax credits.

How much does private student loan debt cost?

Private student loans have become increasingly popular among college students looking to fund their education at any cost. However, these loans can often become a burden rather than a benefit if you do not pay them back in full after graduation. Private student loans fall under federal regulations, meaning they carry special interest rates, fees, and terms. Once you graduate, you may need to work several years before making a payment. Then, once you make a payment, you still have the potential to incur additional fees throughout the repayment period. Many people even find that they cannot afford to repay at all!

What kind of financial aid do I qualify for?

Many private student loan programs offer borrowers a number of different types of assistance. These options include income-driven plans and repayment plans designed to help those with lower incomes manage costs. Before choosing a program, learn what each plan offers, including how much you could potentially owe over time. Your lender should be able to provide information about both standard and alternative repayment programs.

Is my school eligible for federally guaranteed loans?

Federal student loans are backed by the government, so you don’t need to worry about paying high interest rates or being penalized for defaulting. If you choose to take out a Federal Direct Loan, you will receive a fixed amount based on your expected family contribution (EFC) minus any grants you might receive. You won’t receive a grace period to repay your loan. Instead, payments begin immediately upon receiving the funds. Repayments can continue while working toward a degree, or for as long as 25 years following completion of studies. Because your EFC is determined by factors like your parents’ income, you must prove that you meet certain criteria in order to borrow money.

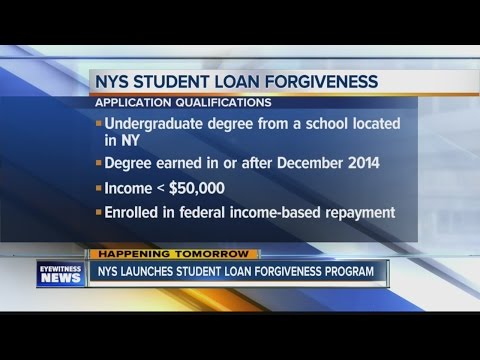

To qualify, your monthly earnings must be less than $50,000 per year plus any other expenses you may have. If you earn more than this threshold, you may be considered ineligible for federal funding. Your federal student loans could also be cancelled for reasons unrelated to your finances. In some cases, the Department of Education will cancel your loans just because it no longer believes that you intend to complete your studies.

Can I consolidate my federal loans?

If you have multiple loans from various lenders, consolidating them into a single loan can save you money on interest charges. Most private student loan programs allow you to combine your loans into one account. The consolidation process involves submitting basic paperwork to the original lenders and then transferring balances between accounts. You’ll never lose access to your existing loans.

As long as you maintain good credit history, you’re likely to get approved for a low-interest rate. And that means you’ll soon break even on the extra savings. A new federal law requires all banks and lenders to disclose to consumers whether they charge higher interest rates to customers who use consolidated loans. To determine eligibility, your EFC must be between $0 and $20,000. If your EFC exceeds this limit, you may not be offered the best rates.

Remember, if you decide to apply for a consolidation loan, you should carefully review all the details before signing anything. Lenders can charge steep fees for processing and closing a loan. Additionally, you might face harsh penalties if your circumstances change, like getting fired or having your wages reduced.

What’s the difference between subsidized and unsubsidized loans?

Unsubsidized private student loans are funded by your own money. You pay the interest directly, and your payments vary depending on your income. On the other hand, subsidized loans are available to those who earn above-median levels. Subsidies cover some portion of the total loan, reducing the interest rate. As long as you remain enrolled in a degree program, you can continue to draw a subsidy until you’ve paid off the entire loan balance. If your enrollment ends or you discontinue classes without completing your program, however, you will no longer receive subsidies.

Which states have laws protecting student loan borrowers?

Nys Student Loans

1.

2.

3. 4. 5.

6.

7.

8.

Nys Student Loans

Nys student loans

Nys student loans were created to help fund college students who want to attend colleges outside of New York State. These loans have some different requirements than federal student aid programs. Students may receive these loans if they meet certain qualifying criteria.

Qualifying Criteria

To qualify for Nys student loans, students need to satisfy several requirements related to their age, income, and financial situation. Age limits are 18-23 years old, with no more than $50,000 in total household assets. Income limits depend on the type of loan and whether the student lives at home.

Loan Types

There are two types of Nys student loans for undergraduates: subsidized and unsubsidized. Subsidized loan amounts vary depending on the school attended. Unsubsidized loans do not change based on the school attended. There are five different loan types, each with its own set of repayment terms and conditions.

Repayment Terms

Repayment terms range from 10 to 20 years. However, monthly payments are determined by the amount borrowed. Loan types include PLUS (parental), Federal Direct (federal), Perkins (state), and FFEL (for those attending for vocational training).

Maximum Amount

The maximum amount of Nys student loans varies depending on the loan type chosen. PLUS loans offer the highest maximum amount at $20,500 per year. For Federal Direct and Perkins loans, the maximum is $10,500. Finally, for FFEL loans, the maximum is between $6,300 and $9,600.

Interest Rates

Interest rates begin accruing as soon as the first payment is due. Depending on the loan type, interest rates range from 4% to 6%. This means that borrowers pay 4% to 6% annually on all outstanding balances.

Monthly Payments

Monthly payments vary depending on the loan type. Each type offers a different minimum payment requirement. For instance, PLUS loans require a minimum payment of $100 per month. On the other hand, FFEL loans only require a monthly payment of $40.

Loan Cancellation

Nys student loans can be cancelled after ten years if the borrower does not graduate. If graduated, then they cannot be cancelled until ten years after graduation.

Nys Student Loans

What is an Nys Loan?

An Nys loan is a federal student loan program that’s administered by the U.S. Department of Education. With an Nys loan, you have a choice of repayment plans based on income and family size. You may repay your loans over five years, seven years, 10 years or any combination thereof.

Is Nys Student Debt Different Than Other Federal Student Loans?

Yes! There are a few differences between federal student loans and Nys student loans. First, with Nys loans you don’t get a fixed interest rate. Instead, the interest rate is determined by the yield spread premium (YSP) index, which is based upon the difference between Treasury bill rates and treasury bonds. The higher the YSP, the lower the interest rate. Also, Nys loans are not dischargeable in bankruptcy unless they were obtained by fraudulent means. Finally, unlike federal student loans, which can only be paid back if borrowers earn at least half time, you can repay Nys loans even if you only make minimum wage.

How Do I Apply For An Nys Loan?

The application process for Nys loans is simple. You go online at www.nslds.ed.gov and fill out a short form. Once you apply, you’ll need to provide tax returns for the last two years and proof of financial responsibility. In addition, you will need to submit documentation showing that you earned less than $50,000 per year during those two years. If you qualify, you’ll receive your first disbursement within 30 days.

►HEY, we’ve got more valuable information here: ►CLICK HERE LOANS FOR STUDENTS◄

►Cloud of related items ▼

bloque1x

Related Links ▼

- Studentaid.gov/understand-aid/types/loans

- Salliemae.com/student-loans/

- Discover.com/student-loans/

- Nerdwallet.com/best/loans/student-loans/private-student-loans

- Money.usnews.com/loans/personal-loans/personal-loans-for-students

- Credible.com/blog/student-loans/personal-loans-for-students/

- Govloans.gov/categories/education-loans/

- Forbes.com/advisor/student-loans/best-private-student-loans/

- Navyfederal.org/loans-cards/student-loans.html

- Wellsfargo.com/goals-going-to-college/loan-options/

- Whitehouse.gov/briefing-room/statements-releases/2022/08/24/fact-sheet-president-biden-announces-student-loan-relief-for-borrowers-who-need-it-most/

- Ed.gov/category/keyword/federal-student-loans

- Myfedloan.org/

- Navient.com/

- Usa.gov/student-loans