I’m not sure if I’ll make any money off this video, but I hope you guys enjoy! ^_^

Drain Cleaner – Do You Use One?? How To Get Rid Of Stains In Your Tubs!!

Drain cleaning vs drain augurting – what’s the difference??? What should you do about clogs in toilets and sinks, drains etc. at home? Hope this helps 🙂

Net Student Loans

Net student loans

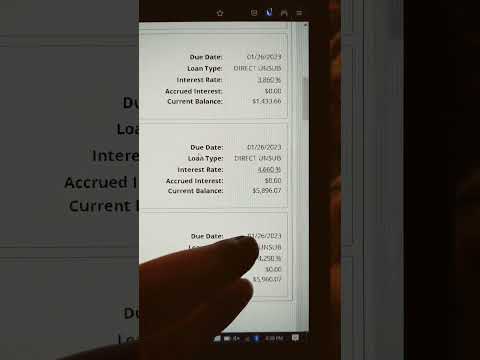

The average yearly cost of college is $10,800. But that doesn’t mean that everyone has to pay that much. In fact, only half the students who go to school actually end up paying off their loan debt. And if you’re making $25,000 or less per year, then you may qualify for financial aid. You can get grants, scholarships, and work-study programs. Here’s how to figure out what kind of student loans you have and where they stand. First, take a look at your federal student loans. Most people don’t realize these are called “net,” not “gross.” Gross means the total amount you owe. Net means what you still owe after taking into account all forms of financial aid received. Next, check what state you live in. Your state may provide scholarships and grants. Lastly, check out any private scholarships or grants you have available to you. Now, remember – there’s no need to worry about private student loans right now. Let’s say you had a job offer from another company right now. If you accepted that offer, you’d likely have to quit school. But let’s say the employer agreed to defer repayment until you graduate. That would be considered a private loan.

Private student loans

Private student loans are those that do not belong to anyone else. Usually, they’re held by banks or credit unions. Private student loans are often used for tuition, room and board, books, supplies, equipment, and transportation. Unlike federal student loans, private student loans don’t require income verification. However, the interest rate on private loans tends to be higher than public ones. How do I know if my private student loans are going to be paid back? Well, according to the U.S. Department of Education, private student loans are usually deferred until graduation or dropout. But again, the interest does accrue. And there’s a chance that even though you earn enough money to make payments, the bank might choose not to make them. So, if you have private student loans, talk to your lender. See if he’ll agree to give you a break on your payment schedule. Be prepared to negotiate.

Net Student Loans

Who gets student loans?

Student loans are given out to people who want to continue their education after high school, whether they go to college, technical schools, trade schools, etc. Student loans are often needed if you do not have enough money to pay for tuition upfront. You may get the loan at any time throughout your life. Most people take out student loans right after graduating from college and are then paying them off for 30 years. If you don’t graduate college, you’ll still need to repay these loans, just until you’re older than 18.

How much do student loans cost?

You might think that most people would only borrow what they need to cover the cost of tuition. However, the government says that the average borrower takes out $28,000 per year. That’s about $904 per month! And that doesn’t even count private lenders, who charge higher rates. So, if you’re thinking about going to school, make sure you know how much you will need before you apply.

Do I have to pay back my student loans?

When you first start repaying your student loans, you won’t have to pay anything else except interest. But you’ll eventually have to start making monthly payments. Once you’ve paid for a certain amount of time (usually 10-25 years), your remaining balance becomes forgiven.

What happens to my loan if I die?

If you die while you’re still repaying your student loans and haven’t repaid everything you owe, you will leave behind unpaid bills and creditors. Your family members might have to deal with this debt, too.

Can I find out how much I owe?

Yes! Every few months, the federal government sends you a bill called a “statistical summary.” You can see exactly how much you owe and where you stand in terms of repayment.

Should I refinance my student loans?

This is something you should talk to your lender about and consider carefully before deciding. Refinancing your student loans could lower your monthly payment, and some companies offer 0% APR for a set period of time. Make sure you understand all the details of refinancing and if it makes sense for you.

Where can I find out more information about student loans?

Net Student Loans

What are student loans?

Student loans are money borrowed by students to cover the costs involved with attending school and getting their degrees. These loans are taken out over many years while they attend college and should be repaid after graduating. Students often take out big amounts of debt when taking out loans, and if they do not pay them back on time, they could end up paying much more than what was agreed upon when they took out the loan.

Why are student loans becoming more expensive?

The cost of student loans have been increasing dramatically ever since the recession began in 2008. Because of this, students who are unable to repay their loans will end up having to go into extreme financial hardships. Many people get forced to make payments for years even after graduation, and some may even default on their loans altogether. There are some things that schools can do to help keep these costs down, though, including lowering tuition rates and making sure that the education received is worth the price paid.

How do I know how much my student loans are going to cost me?

There are different ways that lenders calculate the monthly payment amount for borrowers based on factors like interest rate, type of loan, repayment term, etc. Even though your lender might use one method to figure out your payment, it doesn’t mean that it is right for everyone else. To find out exactly how much you will owe each month, it’s best to contact your lender directly and ask about options that they offer. You may be able to set up automatic payments or simply lower the amount that you pay each month.

Is it possible to stop paying for student loans early?

Yes! If you are enrolled in deferment programs, you can stop repaying your loans before the due date without facing any penalties. Deferments include forbearance, suspension, consolidation, extension, and modification. However, you cannot stop making payments entirely until three months later. After that, you will start accruing additional fees and fines if you don’t continue to make payments.

Can I apply for income-based repayment plans?

If you qualify for income-based repayment, you won’t need to worry about paying off your student loans at all. Instead, you would just need to make smaller payments each month. The size of those payments will depend on how much you earn, but whether or not your payments are being subsidized by the government will determine whether or not you qualify for that plan. 6. Will my Social Security benefits affect my student loan payments?

Social security payments are taxable, meaning that they will count towards your total yearly income for purposes of calculating your taxes. As long as you file a tax return, however, you shouldn’t have any problems with paying taxes on your social security. Your student loans should remain separate from your social security payments and won’t be affected by changes in either of them.

Where do student loans fall under bankruptcy?

Most private student loan companies aren’t included in consumer bankruptcy proceedings. Private creditors, however, do have the opportunity to pursue collections actions once a borrower files for bankruptcy. Some types of debts, like medical bills, are generally excluded from bankruptcy protection.

Net Student Loans

Do I qualify?

If you’re looking to get Net Student Loan forgiveness, you need to have taken out at least $50k worth of student loans over the past 10 years. Your income doesn’t matter – whether you make $100k or $10k, if you’ve earned enough money to pay back your student loan debt (which you’ll know if you’ve borrowed $50k over the last 10 years), then you may be able to apply for forgiveness.

How much do I owe?

You don’t actually have to have paid off your entire student loan balance before applying, however your best bet is to aim to have repaid at least 50% to receive 100% benefit. If you’re planning to stop paying your student loans once you get forgiven, then aiming to repay at least 25-35% of your total debt could help you reach that goal faster.

What’s the application process?

To start, you’ll need to complete a Free Application for Federal Student Aid(FAFSA). You’ll also need to provide proof of your earnings and identify how much you owe. Once you submit your FAFSA, the government will give you information about how much you may qualify for based on your financial situation.

When do I apply?

The sooner you apply, the better! Most students should apply for their federal student aid early in their academic career – between the beginning of August and December. If you wait until after January 1st, your chances of receiving funding decrease dramatically.

What happens if I’m accepted?

Once you’re approved, you’ll be issued an award letter that gives you details regarding what programs you qualify for, your eligibility requirements, and any documentation you’ll need to submit.

►HEY, we’ve got more valuable information here: ►CLICK HERE LOANS FOR STUDENTS◄

►Cloud of related items ▼

bloque1x

Related Links ▼

- Studentaid.gov/understand-aid/types/loans

- Salliemae.com/student-loans/

- Discover.com/student-loans/

- Nerdwallet.com/best/loans/student-loans/private-student-loans

- Money.usnews.com/loans/personal-loans/personal-loans-for-students

- Credible.com/blog/student-loans/personal-loans-for-students/

- Govloans.gov/categories/education-loans/

- Forbes.com/advisor/student-loans/best-private-student-loans/

- Navyfederal.org/loans-cards/student-loans.html

- Wellsfargo.com/goals-going-to-college/loan-options/

- Whitehouse.gov/briefing-room/statements-releases/2022/08/24/fact-sheet-president-biden-announces-student-loan-relief-for-borrowers-who-need-it-most/

- Ed.gov/category/keyword/federal-student-loans

- Myfedloan.org/

- Navient.com/

- Usa.gov/student-loans