This topic was d by the question,”What is the interest rate of federal student loans?”

Answer: Interest rates on federal student loans range between 2% – 8%, depending on the loan type. Interest accrues monthly and is paid back at the end of each month while you’re enrolled in school. You’ll need to repay your loans whether you graduate or not. As long as you have a job, federal student loans can be discharged after 20 years regardless if you make payments or not. If you don’t have a job, they can be discharged after 10 years.

The average interest rate for federal student loans was 6.21 percent for the 2015-2016 school year, according to the U.S. Department of Education. That’s down slightly from 6.24% in 2014-2015.

If you’re looking at private loans, they come with their own set of terms and costs. And don’t forget about your state grants!

Interest Rate Of Federal Student Loans

Interest Rates on Federal Student Loan

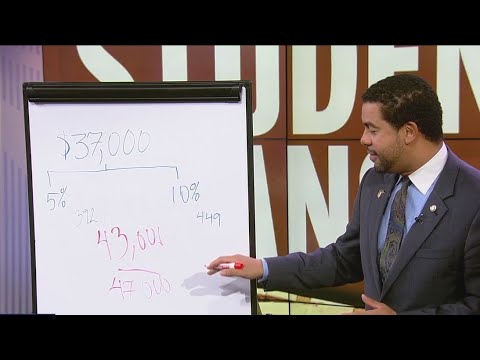

The interest rates on federal student loans have increased since July 1st 2018. The rate increased from 2.86% to 3.86% percent APR.

For those who borrow $10,000 in undergraduate education costs, this means you’ll pay about $35 more per month.

However, if you take out private student loan, the interest rate goes down to 6%.

Why Does Student Loan Interest Increase?

Student loans are an investment that gives back over time. When the interest rates increase, borrowers have access to more capital and can use the money toward their debt payments. However, some students may choose not to repay their loans because they think the interest rates will decrease after the grace period ends.

According to the U.S. Department of Education, interest rates are set by Congress and the Executive Branch of government.

How Can You Avoid Paying More On Your Student Loan?

You can avoid paying more on your student loan by making the best financial decisions early on in your college career.

Choose a school where your expected graduation date is close, especially if you plan to pursue a graduate degree. If you find yourself struggling financially, consider taking out smaller amounts of student loan than what you originally planned.

If you decide to apply for a consolidation loan, make sure you do not consolidate at the same time you apply for a private student loan. Consolidating two different types of loans at once could result in higher monthly payment.

Also, look closely at how much additional interest you would pay by consolidating your loan. If you’re able to get a lower interest rate by consolidating, that’s a good thing. But if you end up having to pay more interest, remember to always ask yourself “Is this worth it?”

Interest Rate Of Federal Student Loans

The interest rate on student loans rose again last week — to 6.21 percent. That’s a significant jump since July 2014 — just two years ago. But don’t worry about it. You’re not going to have to pay any more than 6 percent this year. Here’s how it works…

If you borrowed $10,000 in July 2015 and paid 10 percent annual interest, you’d owe $11,600 at the end of 2016. If Congress had increased the interest rate, say, to 12 percent, you would’ve owed $12,800. So what happened? The federal government raised the interest rate on subsidized Stafford loans – those given to students who qualify for low-cost federal financing – from 5.31 percent to 6.21 percent effective July 1. And the rates on unsubsidized Stafford loans – those given out to everyone else – went up from 4.21 percent to 5.41 percent. Which means that in real terms, the rate on subsidized Stafford loans hasn’t changed since July 2013. Subsidized Stafford loan rates are based on the yield on Treasury bills, which were 2.25 percent in December 2012. So even though they’re now higher, they haven’t actually gone up much.

In fact, according to data compiled by the College Board, the average monthly payment on an undergraduate student loan remains below the amount borrowers owed back in 2013. In December 2013, the average repayment was $318 per month; last August, it was $335.

There’s no question that student debt is a serious problem. According to the Institute for College Access & Success, 44 million Americans hold some kind of student loan debt. About half of them owe less than $25,000. But many borrow more than twice that amount. And while high school graduates owe an average of $26,500, college grads owe nearly $40,000.

The good news is that the interest rates on subsidized Stafford loans won’t change until 2019. That’s when a full decade passes after the current six-year clock runs out. Meanwhile, unsubsidized Stafford loan rates won’t go up above the 6.8 percent cap set by law until July 2018, when the clock expires on the current four-year limit. By then, however, we’ll hopefully be talking about whether to extend the debt ceiling, not raising it.

So if you’re currently paying the maximum 6.21 percent on your subsidized Stafford loan, you can breathe easy. Your payments won’t get any higher. For everyone else, however, the bad news is that your interest rate is now officially set in stone. From now until July 2018, you’ll continue to pay the same amount of money each month whether Congress raises the interest rate or not. And it’s possible that the rates could increase further over the coming months. As I mentioned before, the Department of Education announced this week that it anticipates approving new applications for unsubsidized Stafford student loans starting January 8. At this point, there’s no telling where those rates will wind up.

But let’s assume for the sake of argument that nothing changes between now and July 2018. Then, assuming you still have the same job and income level, here’s how your payments might look. If you borrowed $20,000 in July 2015, you’d owe $23,900 at the end of 2017. If Congress increases the interest rate to 6.9 percent, you’d owe $24,800. And if you borrowed $30,000, you’d owe $33,700 in late 2017. (Remember, these calculations are based on the assumption that the interest rate doesn’t change.)

And yes, you should probably put off taking out new loans until sometime later. Even with the lower rates, borrowing is expensive. The average borrower pays about $1,200 in interest annually. That’s more than double the amount of the original loan principal. When you factor in the tax advantages of making education investments now instead of later, it makes sense to borrow only what you absolutely need.

Interest Rate Of Federal Student Loans

Borrowers with federal student loans who have not yet begun repaying their loan, on average, pay about $4 per day in interest. That’s 0.25 percent of their monthly payment amount. If borrowers have already started making payments, they’re paying $8 per day in interest, which amounts to 1.5 percent of their monthly payment. For private student loans, borrowers with those kinds of loans pay an average of 4 percent of their monthly payment in interest.

When comparing interest rates between federal loans and private loans, remember to keep in mind how much students owe before their loans start accruing interest. Federal student loans generally don’t begin charging interest until after a borrower graduates and starts repaying his/her loan. Private student loans, however, generally start charging interest right away.

There are several types of federal student loans. Direct Subsidized Loans are government-backed loans that allow students to borrow money while still enrolled at least half time. (The government pays the interest on these loans.) Undergraduate Deferred Loans are similar to direct subsidized loans except that borrowers must graduate, get employment, and begin repaying their loans before they will start paying interest. Graduate Plus Loans are guaranteed by the Department of Education but aren’t backed by the U.S. Treasury. These loans cannot be discharged in bankruptcy. Private student loans are generally not guaranteed by the U.S Government, although some private lenders offer insurance protection if a borrower defaults.

Students who take out both federal and private student loans may find themselves in a bad position because they’ll end up with two different sets of terms, conditions, and interest rates.

Most borrowers take out both federal and non-federal student loans simultaneously. In order to do this, they need to create a single loan package, which means bundling together all their student loan information and paying a higher interest rate than they would pay if they took out separate loans.

After graduation, a borrower who takes out only federal student loans can consolidate her/his loans under the William D. Ford Direct Loan Program. A borrower should apply for consolidation only once she/he has graduated, gotten employed, and started making payments on the loan(s). To qualify for consolidation, a borrower’s repayment plan must have been set to 12 months or less when he or she applied for consolidation.

When a borrower consolidates loans, he/she gets a single loan balance, low monthly payments, and lower interest rate. However, borrowers who consolidate loans must make three minimum monthly payments instead of just one. While a loan consolidation lowers the amount of interest paid over time, it does increase the total amount of interest borrowed.

In addition to loan consolidation, a borrower can refinance her/himself into a lower interest rate loan. This is called refinancing. Refinancing, unlike loan consolidation, doesn’t eliminate the original debt or reduce the principal owed. Instead, borrowers use the proceeds from a loan refinancing to pay off their existing loan(s) and then take out a new loan with a lower interest rate.

On average, a borrower with a federal education loan can expect to save about $200 each month by refinancing.

A borrower who wants to minimize the cost of college can look into taking out a federal Perkins Loan. A loan granted by the National Association of State Universities and Land-Grant Colleges (NASULGC), it requires a good credit history.

A borrower can also consider a PLUS Loan, which is a type of private student loan. PLUS Loans require a co-signer, like a parent, relative, friend, or employer.

Lastly, students can opt to go without any student loans or simply use public assistance programs like Pell Grants. Public aid programs like these provide grants based on financial need rather than merit or credit score.

According to the Consumer Financial Protection Bureau, borrowers with federal student loans can submit a complaint to the bureau, the department of education, or their lender if they believe they were mistreated or misled when signing up for or applying for a student loan.

If you have any questions regarding your federal student loans, contact your school’s financial aid office. If you’d prefer to speak with someone else, call the Department of Education’s toll-free helpline at 877-433-7322.

►HEY, we’ve got more valuable information here: ►CLICK HERE LOANS FOR STUDENTS◄

►Cloud of related items ▼

bloque1x

Related Links ▼

- Studentaid.gov/understand-aid/types/loans

- Salliemae.com/student-loans/

- Discover.com/student-loans/

- Nerdwallet.com/best/loans/student-loans/private-student-loans

- Money.usnews.com/loans/personal-loans/personal-loans-for-students

- Credible.com/blog/student-loans/personal-loans-for-students/

- Govloans.gov/categories/education-loans/

- Forbes.com/advisor/student-loans/best-private-student-loans/

- Navyfederal.org/loans-cards/student-loans.html

- Wellsfargo.com/goals-going-to-college/loan-options/

- Whitehouse.gov/briefing-room/statements-releases/2022/08/24/fact-sheet-president-biden-announces-student-loan-relief-for-borrowers-who-need-it-most/

- Ed.gov/category/keyword/federal-student-loans

- Myfedloan.org/

- Navient.com/

- Usa.gov/student-loans