Student loans are often thought of as being unsecured debt; however, they are actually secured by the government’s guarantee that you repay them if you want to attend college. Your federal student loan servicer (the company that handles collections) may not accept cosigners. Check out our article about how to use private lenders for student loans.

If your Federal Family Education Loan Program (FFELP) borrower has defaulted, ask yourself if you would feel comfortable cosigning for him/her. You’ll probably find that you don’t have any desire to do so. If you do decide to make a commitment, your best bet is to get a private lender to co-sign the loan for you. Many students choose to take advantage of private student loan options that allow them to borrow money without having their credit score negatively impacted. To learn more, visit PrivateLenders.org.

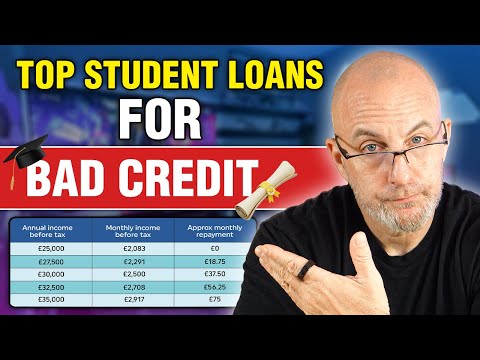

While you’re looking at student loan options, be sure to look at the repayment plan available to you. The longer you leave a loan unpaid before making payments, the higher the interest rate that you’ll pay.

Learn from your mistakes and avoid committing to something you cannot afford. Don’t let your dreams of going to school become a burden. Keep your financial situation under control by doing some research and planning ahead.

Student Loans Bad Credit With Cosigner

Student Loans

If you have student loans, they may not seem bad at first glance. You go to school, get good grades, get a job after graduation, and pay off the loan in full. But these are the same reasons why people find themselves in debt trouble later in their lives. If you want to save money, don’t take out student loans. There are cheaper ways to fund your education.

Cosigning Loan

If you have student loan debt, then having someone else cosign your loan might help you reduce the amount you owe. A cosigner is basically your partner in crime who takes responsibility for paying back any portion of the student loan if you default on your payments. In some cases, cosigners have to pay interest and principal along with you.

Financial Aid

You may think financial aid means free money, but the reality is that many colleges offer scholarships based on need. Also, you may qualify for federal grants based on your family income level. Take advantage of every opportunity. Many schools even offer merit-based scholarship opportunities.

Job Opportunity

When looking for jobs, keep in mind how much debt you would incur if you work in certain fields. Law firms pay over $100k per year. Doctors make around $200k per year. Dentists make about $160k per year. Not only do those salaries look great, but they give you something to fall back on if you run into trouble with your loans.

Tax Refund

Finally, tax refunds are another way to save. Student loan companies report to the IRS that you had a refund each year. When filing taxes, the government reports your total refunds. So if you received a $2,000 refund, your lender would report as receiving $2,000 less than what was actually deposited into your account. This puts less pressure on your budget.

Student Loans Bad Credit With Cosigner

Student loans are one of the best ways to finance your education. They’re great if you have a high-paying job waiting for you after graduation, especially since you’ll pay only interest while you work. But no matter how good your job prospects look at the end of college, chances are they won’t pay enough to cover your student loan debt once you graduate. That’s where cosigning comes in. A cosigner is someone who agrees to help out with paying off your student loans. By doing so, he or she becomes personally responsible for repaying those loans. And just like if you co-signed your parents’ car loan, you could lose everything — including their home — if you default on your student loans. So before you go cosigning, make sure you understand what happens if you don’t repay or default on your own loans.

If you cosign, your credit score may take a hit. Since you’ll be responsible for any unpaid balances on your student loans, lenders will report your account balance to credit bureaus. You can expect to see your FICO scores drop about 50 points each time you miss a payment. After three late payments, your scores may even fall further than 100 points. To prevent this from happening, make sure you keep your cosigned accounts current and avoid missing payments altogether.

If you get fired or laid off from your job, your cosigner may not be able to cover your losses, either. If you default, your cosigner doesn’t automatically become liable for your debts. Instead, your cosigner might try to collect money from you or sue you. In order to protect yourself, you should always ask your employer whether they’ll continue covering your bills if you get laid off or fired. If they aren’t willing to do so, you shouldn’t sign anything until you find a new job.

Your cosigner may never know you have trouble repaying them. When your loan servicer sends you statements, they’ll list all your cosigners under your name, instead of theirs. Even though the cosigner may have agreed to be responsible for your loans, lenders aren’t obligated to let him or her know about it. Instead, they send letters directly to you and your cosigner, asking for repayment. If your cosigner finds out about the letter and asks you about it, you can say that you didn’t receive notice of the bill and weren’t aware of its existence.

You might owe more than you thought. According to NerdWallet, students who co-sign a loan often assume they’ll only have to pay 20% of the total balance. But depending on state law, some states allow cosigners to be held responsible for as much as 50%, 60% or even 70% of the debt. These percentages can increase up to 80% in some cases. Plus, these rates can change based on the length of time the loan remains delinquent.

You may not qualify for federal student aid. Before signing anything, make sure you understand

Student Loans Bad Credit With Cosigner

Student loans bad credit with cosigner are not uncommon among students today. There are many factors that have caused this phenomenon. One major factor is that student loan providers are now able to offer several kinds of financial assistance, including grants and scholarships. Students who do not qualify for these types of help often turn to their parents for money. Another cause is that most colleges and universities require a co-signer on any type of financial aid package. If a parent does not have good credit, he may choose to pay for the debt rather than risk having his name attached to a student loan.

Because of the rise in the popularity of private student loans, the average amount that a student borrows has increased significantly over the last few years. In 2009, students borrowed an average of $9,000 per year; however, according to the New York Fed’s Consumer Credit Panel, student loan borrowing topped out at almost $20,000 in 2011. This is quite a jump considering the fact that in 2001, just two years before the economy collapsed, student loan borrowing was only about $8,500. That is a lot of money for someone without a job. To make matters worse, most student loans are non-dischargeable under bankruptcy law. Even if a person manages to get rid of his debts completely, he will still be saddled with them for the rest of his life.

As long as the borrower is willing to pay back the amount owed, student loans are generally considered to be a relatively safe way to finance college education. However, since the interest rates charged on federal student loans is currently at its highest level ever, borrowers should be aware that they could end up paying much more than they expected. When the rate is set below 5 percent, borrowers can expect to pay between 1 and 2 percent just to cover the cost of funding the loan. On the other hand, when the rate hits 6.5 percent, the annual interest cost rises to around 4 percent. According to some experts, a student loan rate of 8 percent would be more than enough to deter even highly qualified individuals from going to school.

Most student loans are paid off after five years of payments. But what happens if a person doesn’t complete the payment plan? Defaulting on a student loan isn’t always a bad thing. If a person defaults on a mortgage, default insurance charges are added onto the principal balance and the monthly payment goes down proportionately. A person who defaults on a student loan pays the interest that accrues on the unpaid portion of the loan. It is also possible to refinance a student loan once the borrower is in default.

There are several ways to avoid defaulting on a student loan. All borrowers who find themselves in the middle of a personal financial hardship should contact their lender first. If that fails, they should try to negotiate with creditors directly. Otherwise, if no agreement can be reached, they should start looking for alternatives. These options include deferment programs, forbearance programs, and consolidation. Student Loan ForbearanceA forbearance program is similar to a deferral program but does not entail making smaller payments each month instead of none at all. Instead, it allows the borrower to stop making payments entirely until the situation has improved. While some states provide low income forbearance programs that allow people to postpone repayments while receiving social services, there are also federal forbearance programs that are open to everyone regardless of income. In order to qualify for a forbearance program, a borrower must file a request with his lender. He may then ask to have his loan payment suspended until a certain date in the future. However, he cannot use this program as an excuse to delay repayment indefinitely. Borrowers who take advantage of forbearance programs often feel guilty about it later because they know they could have avoided repaying their debt had they chosen not to pause their payments. Additionally, forbearances aren’t always affordable. Many federal and private lenders charge higher interest rates on those who apply for them.

Student Loans Bad Credit With Cosigner

If you are planning to get student loans, make sure to check if you have any cosigners! There are many people who are willing to help you out financially, but they don’t know anything about the loan process. So, if you don’t want to damage their credit score, then you should not take out any loans without them knowing about it. 2. If you’re going to work while getting student loans, then try to find something that’s only going to last you until your graduation date. Don’t use your student loans to pay for things that won’t benefit you at all! You may think that you need that car or that apartment right now, but after graduation, do you really need those things? 3. Find out what kind of interest rate you’ll be paying on your student loans before taking them out. That way, you know exactly how much money you’ll owe over time. 4. Make sure to read everything carefully before signing anything. If you aren’t sure about anything, ask someone else to look over your paperwork. 5. Take advantage of the money-saving programs that your school offers. Many schools offer scholarships and grants for students who need financial assistance. 6. Try not to forget about your payments! That means keeping track of everything on your monthly budget. If you miss a payment, it could cause problems down the road. 7. Remember that you’ll be paying off your loans for decades to come, so plan accordingly. 8. If you’re having trouble making ends meet, consider using your parents’ accounts for a short period of time. Your parents might not mind helping you out, and this can give you some extra cash to buy food or gas. 9. If you’re not enrolled in college yet, save up as much as possible. Then go back to school once you graduate. 10. A lot of people find themselves in bad situations due to unexpected events, but you shouldn’t let that stop you from getting ahead. 11. Even though student loans are great because you don’t have to worry about repaying them when you graduate, they can still haunt you for years to come. 12. Just because you’re thinking about getting student loans doesn’t mean you have to get them! If you don’t need them, you probably don’t need them. 13. Don’t try to borrow too much money. You don’t want to put yourself in debt just because you want to live the lifestyle you desire. 14. Don’t rush into applying for student loans. If you apply early enough, you could actually get a lower interest rate. 15. When applying for loans, always make sure to keep copies of everything that is sent to you. If you lose or forget something, you’ll never be able to get a refund. 16. Most banks require a cosigner when you apply for a loan. 17. Paying off your student loans isn’t the end; it’s the beginning! 18. Always double-check your student loan paperwork

►HEY, we’ve got more valuable information here: ►CLICK HERE LOANS FOR STUDENTS◄

►Cloud of related items ▼

bloque1x

Related Links ▼

- Studentaid.gov/understand-aid/types/loans

- Salliemae.com/student-loans/

- Discover.com/student-loans/

- Nerdwallet.com/best/loans/student-loans/private-student-loans

- Money.usnews.com/loans/personal-loans/personal-loans-for-students

- Credible.com/blog/student-loans/personal-loans-for-students/

- Govloans.gov/categories/education-loans/

- Forbes.com/advisor/student-loans/best-private-student-loans/

- Navyfederal.org/loans-cards/student-loans.html

- Wellsfargo.com/goals-going-to-college/loan-options/

- Whitehouse.gov/briefing-room/statements-releases/2022/08/24/fact-sheet-president-biden-announces-student-loan-relief-for-borrowers-who-need-it-most/

- Ed.gov/category/keyword/federal-student-loans

- Myfedloan.org/

- Navient.com/

- Usa.gov/student-loans